Your Success, Our Mission!

6000+ Careers Transformed.

Joint distributions and covariance are essential concepts in probability theory and statistics. The joint distribution of random variables is the probability distribution of a set of random variables, whereas covariance measures the degree to which two random factors change together.

Joint distributions are probability distributions that describe the relationship between two or more random variables. A joint distribution specifies the probability of each possible combination of values for the random variables. The joint probability density function (PDF) for two continuous random variables X and Y is denoted as f(x, y), while for two discrete random variables X and Y, it is denoted as P(X = x, Y = y).

Example: Suppose we have two random variables X and Y that represent the number of heads and tails, respectively, in two coin flips. The joint distribution of X and Y can be represented as follows:

Example: Suppose we have two random variables X and Y that represent the number of heads and tails, respectively, in two coin flips. The joint distribution of X and Y can be represented as follows:

| X/Y | 0 | 1 | 2 |

|---|---|---|---|

| 0 | 1/4 | 1/2 | 1/4 |

| 1 | 1/2 | 0 | 1/2 |

| 2 | 1/4 | 1/2 | 1/4 |

Marginal distributions refer to the probability distributions of individual random variables obtained from a joint distribution. The marginal distribution of X is obtained by summing (in the discrete case) or integrating (in the continuous case) over all possible values of Y.

Example: Using the joint distribution from the previous example, the marginal distribution of X can be obtained as follows:

| X | 0 | 1 | 2 |

|---|---|---|---|

| P(X) | 1/4 + 1/2 + 1/4=1/2 | 1/2 + 1/2=1 | 1/4 + 1/2 + 1/4=1/2 |

Conditional distributions portray the probability distribution of one irregular variable given the esteem of another. The conditional conveyance of Y given X is indicated as P(Y | X) or f(Y | X), and is calculated by dividing the joint distribution of X and Y by the marginal distribution of X.

To find the conditional probability of X given Y, we need to use the formula:

P(X|Y) = P(X and Y) / P(Y)

Illustration:

Utilizing the joint dissemination from the past illustration, the conditional distribution of Y given X=1 can be gotten as follows:

Let's find the conditional probability of X = 1 given Y = 2:

P(X=1|Y=2) = P(X=1 and Y=2) / P(Y=2) P(X=1 and Y=2) = 1/2 (from the table) P(Y=2) = 1/4 + 1/2 + 1/4 = 1 (sum of probabilities in the Y=2 column)

Therefore,

P(X=1|Y=2) = (1/2) / 1 = 1/2

So the conditional probability of X=1 given Y=2 is 1/2.

Covariance measures the degree to which two random variables X and Y are linearly related. It is defined as the expected value of the product of the deviations of X and Y from their respective means:

cov(X,Y) = E[(X - E[X])(Y - E[Y])]

Correlation is a standardized version of covariance, and measures the degree of linear association between two variables X and Y:

corr(X,Y) = cov(X,Y) / (std(X) * std(Y))

Example:

To find the covariance and correlation between X and Y, we need to use the following formulas:

Cov(X,Y) = E[XY] - E[X]E[Y] Corr(X,Y) = Cov(X,Y) / (SD(X) * SD(Y))

where E[XY] is the expected value of the product of X and Y, E[X] and E[Y] are the expected values of X and Y, SD(X) and SD(Y) are the standard deviations of X and Y, respectively.

Let's start by finding the expected values of X and Y:

E[X] = 0*(1/4) + 1*(1/2) + 2*(1/4) = 1 E[Y] = 0*(1/2) + 1*(1) + 2*(1/2) = 1

Next, let's find the expected value of XY:

E[XY] = 00(1/4) + 01(1/2) + 02(1/4) + 10(1/2) + 11(0) + 12(1/2) + 20(1/4) + 21(1/2) + 22(1/4)

= 0 + 0 + 0 + 0 + 0 + 1 + 0 + 2 + 1 = 4/2 = 2

Now, let's calculate the standard deviations of X and Y:

SD(X) = sqrt(E[X^2] - (E[X])^2) = sqrt(0*(1/4) + 1*(1/2) + 4*(1/4) - 1^2) = sqrt(1/4) = 1/2 SD(Y) = sqrt(E[Y^2] - (E[Y])^2) = sqrt(0*(1/2) + 1*(1) + 4*(1/2) - 1^2) = sqrt(3/2)

Now, we can calculate the covariance between X and Y:

Cov(X,Y) = E[XY] - E[X]E[Y] = 2 - (1)*(1) = 1

Finally, we can calculate the correlation between X and Y:

Corr(X,Y) = Cov(X,Y) / (SD(X) * SD(Y)) = 1 / ((1/2) * sqrt(3/2)) = sqrt(8/3)

So the covariance between X and Y is 1 and the correlation between X and Y is approximately 1.63299.

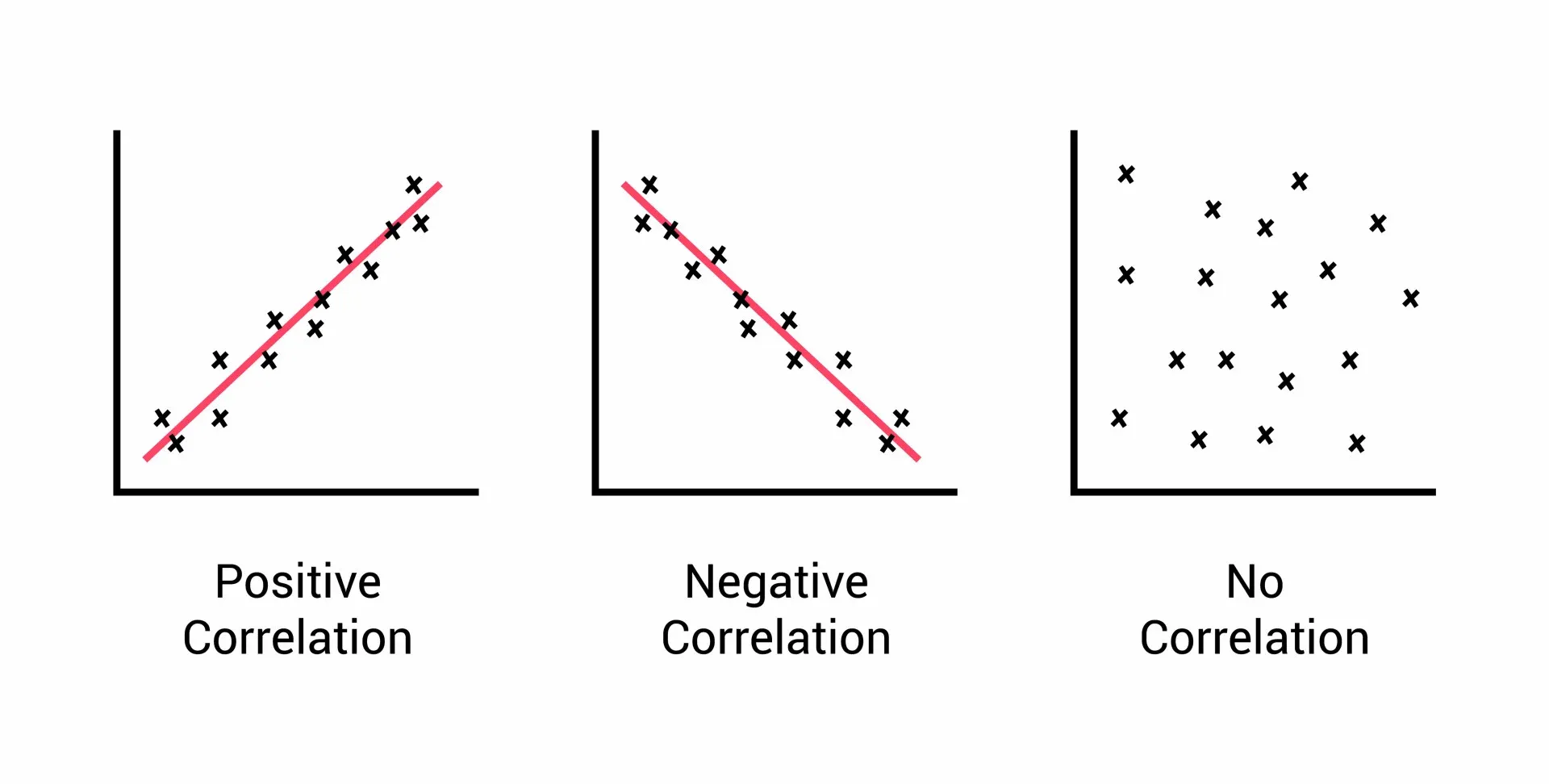

Correlation is a statistical measure used to determine the degree to which two variables are related to each other. Correlation can be either positive or negative, indicating the direction of the relationship between the variables. A positive correlation means that as one variable increases, the other variable also increases, while a negative correlation means that as one variable increases, the other variable decreases.

There are three main types of correlation: positive correlation, negative correlation, and zero correlation.

Types of Correlation

Positive correlation occurs when the values of two variables increase or decrease together. For example, there is a positive correlation between the amount of exercise people do and their level of fitness. The more exercise people do, the fitter they are likely to be.

The formula for calculating the Pearson correlation coefficient for a positive correlation is:

r = (nΣxy - ΣxΣy) / sqrt[(nΣx^2 - (Σx)^2)(nΣy^2 - (Σy)^2)]

where:

Negative correlation occurs when the values of two variables move in opposite directions. For example, there is a negative correlation between the amount of time people spend watching TV and their level of physical activity. The more time people spend watching TV, the less physically active they are likely to be.

The formula for calculating the Pearson correlation coefficient for a negative correlation is:

r = (nΣxy - ΣxΣy) / sqrt[(nΣx^2 - (Σx)^2)(nΣy^2 - (Σy)^2)]

Where:

Zero correlation occurs when there is no relationship between the two variables. For example, there is no correlation between the color of someone's eyes and their shoe size.

Multivariate distributions generalize joint distributions to more than two random variables.A multivariate distribution indicates the probability distribution of a set of random variables, where each arbitrary variable may have a different probability distribution. A few commonly utilized multivariate dispersions incorporate the multivariate ordinary dispersion, the multinomial distribution, and the multivariate t-distribution.

Illustration: Assume we have three arbitrary factors X, Y, and Z, where X and Y are ceaseless random variables and Z may be a discrete random variable. The joint distribution of X, Y, and Z can be spoken to as takes after:

f(x, y, z) = P(X = x, Y = y, Z = z)

Joint distributions and covariance have numerous applications in statistics, probability theory, and data analysis. They are used in fields such as finance, engineering, biology, and machine learning. Some applications of joint distributions include:

In conclusion, joint distributions, correlation and covariance are essential concepts in probability theory and insights that play a vital part in different applications. They permit us to show the connections between different random variables and measure the degree to which they shift together. From fund to genetics and machine learning, joint distributions and covariance are utilized broadly to analyze information, make forecasts, and educate decision-making.

1. What is the joint distribution of two random variables?

A. The probability distribution of a single random variable

B. The probability distribution of a set of random variables

C. The distribution of the difference between two random variables

D. The distribution of the sum of two random variables

Answer: B

2. What does covariance measure?

A. The degree to which two random variables vary together

B. The degree to which two random variables are independent

C. The standard deviation of a single random variable

D. The probability of observing two random variables together

Answer: A

3. Which of the following measures the strength of the linear relationship between two random variables?

A. Variance

B. Correlation coefficient

C. Standard deviation

D. Mean

Answer: B

4. What is the main application of joint distributions and covariance in finance?

A. Estimating heritability and gene expression levels

B. Modeling the joint probability distribution of signals

C. Modeling the relationship between the returns of different assets in a portfolio

D. Modeling the joint probability distribution of time series data

Answer: C

5. What is the correlation coefficient?

A) A measure of the strength and direction of the linear relationship between two variables.

B) A measure of the strength and direction of the non-linear relationship between two variables.

C) A measure of the probability that two variables are related.

D) A measure of the magnitude of the difference between two variables.

Answer: A) A measure of the strength and direction of the linear relationship between two variables.

6. What is the range of possible values for the correlation coefficient?

A) -1 to 1

B) 0 to 1

C) -∞ to ∞

D) 0 to ∞

Answer: A) -1 to 1

Top Tutorials

Python

Python is a popular and versatile programming language used for a wide variety of tasks, including web development, data analysis, artificial intelligence, and more.

SQL

The SQL for Beginners Tutorial is a concise and easy-to-follow guide designed for individuals new to Structured Query Language (SQL). It covers the fundamentals of SQL, a powerful programming language used for managing relational databases. The tutorial introduces key concepts such as creating, retrieving, updating, and deleting data in a database using SQL queries.

Data Science

Learn Data Science for free with our data science tutorial. Explore essential skills, tools, and techniques to master Data Science and kickstart your career

All Courses (6)

Master's Degree (2)

Fellowship (2)

Certifications (2)